Text-to-image/video models like Midjourney, Imagen3, Stable Diffusion, and Sora can generate aesthetic, photo-realistic visuals from natural language prompts, for example, given “Several giant woolly mammoths approach, treading through a snowy meadow…”, Sora generates:

But how do we know if these models generate what we desire? For example, if the prompt is “The brown dog chases the black dog around a tree”, how can we tell if the model shows the dogs “chasing around a tree” rather than “playing in a backyard”? More generally, how should we evaluate these generative models? While humans can easily judge whether a generated image aligns with a prompt, large-scale human evaluation is costly. To address this, we introduce a new evaluation metric (VQAScore) and benchmark dataset (GenAI-Bench) [Lin et al., ECCV 2024] for automated evaluation of text-to-visual generative models. Our evaluation framework was recently employed by Google Deepmind to evaluate their Imagen3 model!

We introduce VQAScore[Lin et al., ECCV 2024] —a simple yet powerful metric to evaluate state-of-the-art generative models such as DALL-E 3, Midjourney, and Stable Diffusion (SD-XL). VQAScore aligns more closely with human judgments and significantly outperforms the popular CLIPScore [Hessel et al., 2021] on challenging compositional prompts collected from professional designers in our GenAI-Bench [Li et al., CVPR 2024].

Background

While state-of-the-art text-to-visual models perform well on simple prompts, they struggle with complex prompts which involve multiple objects and require higher-order reasoning like negation. Recent models like DALL-E 3 [Betker et al., OpenAI 2023] and Stable Diffusion [Esser et al., Stability AI 2024] address this by training on higher-quality image-text pairs (often using language models such as GPT-4 to rewrite captions) or using strong language encoders like T5 [Raffel et al., JMLR 2020].

As text-to-visual models advance, evaluating them has become a challenging task. To measure similarity between two images, perceptual metrics like Learned Perceptual Image Patch Similarity (LPIPS) [Zhang et al., CVPR 2018] uses a pre-trained image encoder to embed and compare image features, with higher similarity indicating the images look alike. For measuring similarity between a text prompt and an image (image-text alignment), the common practice is to rely on OpenAI’s pre-trained CLIP model [Radford et al., OpenAI 2021]. CLIP includes both an image encoder and a text encoder, trained on millions of image-text pairs, to embed images and texts into the same feature space, where higher similarity suggests stronger image-text alignment. This approach is commonly referred to as CLIPScore [Hessel et al., EMNLP 2021].

Previous evaluation metrics for generative models: Perceptual metrics like LPIPS use a pre-trained image encoder to embed the original and reconstructed images into two 1D vectors, and then compute their distance. As a result, perceptually similar images will have a higher LPIPS score. On the other hand, CLIPScore uses the dual encoders of a pre-trained CLIP model to embed images and texts into the same space, where semantically aligned pairs will have a higher CLIPScore.

However, CLIPScore suffers from a notorious “bag-of-words” issue. This means that when embedding texts, CLIP can ignore word order, leading to mistakes like confusing “The moon is over the cow” with “The cow is over the moon”.

Examples from the challenging image-text matching benchmark Winoground [Thrush et al., CVPR 2022], where CLIPScore often assigns higher scores to incorrect image-text pairs. In general, CLIPScore struggles with multiple objects, attribute bindings, object relationships, and complex numerical (counting) and logical reasoning. In contrast, our VQAScore excels in these challenging scenarios.

Why is CLIPScore limited? Our prior work [Lin et al., ICML 2024], along with others [Yuksekgonul et al., ICLR 2023], suggests its bottleneck lies in its discriminative training approach. The structure of CLIP’s loss function causes it to maximize similarity between an image and its caption and minimize similarity between an image and a small set of unrelated captions. However, this structure allows for shortcut — CLIP often minimizes similarity to negatives by simply recognizing main objects, ignoring finer details. In contrast, we suspect that generative vision-language models trained for image-to-text generation (e.g., image captioning) are more robust because they cannot rely on shortcuts—generating the correct text sequence requires a precise understanding of word order.

VQAScore: A Strong and Simple Text-to-Visual Metric

Based on generative vision-language models trained for visual-question-answering (VQA) tasks that generate an answer from an image and a question, we propose a simple metric, VQAScore. Given an image and a text prompt, we define their alignment as the probability of the model responding “Yes” to the question, “Does this image show ‘{text}’? Please answer yes or no.” For example, given an image and the text prompt “the cow over the moon”, we would compute the following probability:

(P(“Yes” | image, “Does this figure show ‘the cow over the moon’? Please answer yes or no.”) )

VQAScore is calculated as the probability of a visual-question-answering (VQA) model responding “Yes” to a simple yes-or-no question like, “Does this figure show [prompt]? Please answer yes or no.” VQAScore can be implemented in most VQA models trained with next-token prediction loss, where the model predicts the next token based on the current tokens. This figure illustrates the implementation of VQAScore: on the left, the image and question are tokenized and fed into an image-question encoder; on the right, an answer decoder calculates the probability of the next answer token (i.e., “Yes”) auto-regressively based on the output tokens from the image-question encoder.

Our paper [Lin et al., ECCV 2024] shows that VQAScore outperforms CLIPScore and all other evaluation metrics across benchmarks measuring correlation with human judgements on image-text alignment, including Winoground [Thrush et al., CVPR 2022], TIFA160 [Hu et al., ICCV 2023], Pick-a-pic [Kirstain et al., NeurIPS 2023]. VQAScore even outperforms metrics that use additional fine-tuning data or proprietary models like GPT-4 (Vision). These metrics can be grouped into three types:

(1) Human-feedback approaches, like ImageReward, PickScore, and Human Preference Score, fine-tune CLIP using human ratings of generated images. (2) LLM-as-a-judge approaches, like VIEScore, use LLMs such as GPT-4 (Vision) to directly output image-text alignment scores, e.g., asking the model to output a score between 0 to 100. (3) Divide-and-conquer approaches like TIFA, Davidsonian, and Gecko decompose text prompts into simpler question-answer pairs (often using LLMs like GPT-4) and then use VQA models to assess alignment based on answer accuracy.

Compared to these metrics, VQAScore offers several key advantages:

(1) No fine-tuning: VQAScore performs well using off-the-shelf VQA models without the need for fine-tuning on human feedback. (2) Token probabilityis more precise than text generation: LLM-as-a-judge methods often assign similar and random scores (like 90) to most image-text pairs, regardless of alignment. (3) No prompt decomposition: While divide-and-conquer approaches may seem promising, prompt decomposition is error-prone. For example, with the prompt “someone talks on the phone happily while another person sits angrily,” the state-of-the-art method Davidsonian wrongly asks irrelevant questions such as, “Is there another person?”

In addition, our paper also demonstrates VQAScore’s preliminary success in evaluating text-to-video and 3D generation. We are encouraged by recent work like Generative Verifier, which supports a similar approach for evaluating language models. Finally, DeepMind’s Imagen3 suggests that stronger models like Gemini could further enhance VQAScore, indicating that it scales well with future image-to-text models.

GenAI-Bench: A Compositional Text-to-Visual Generation Benchmark

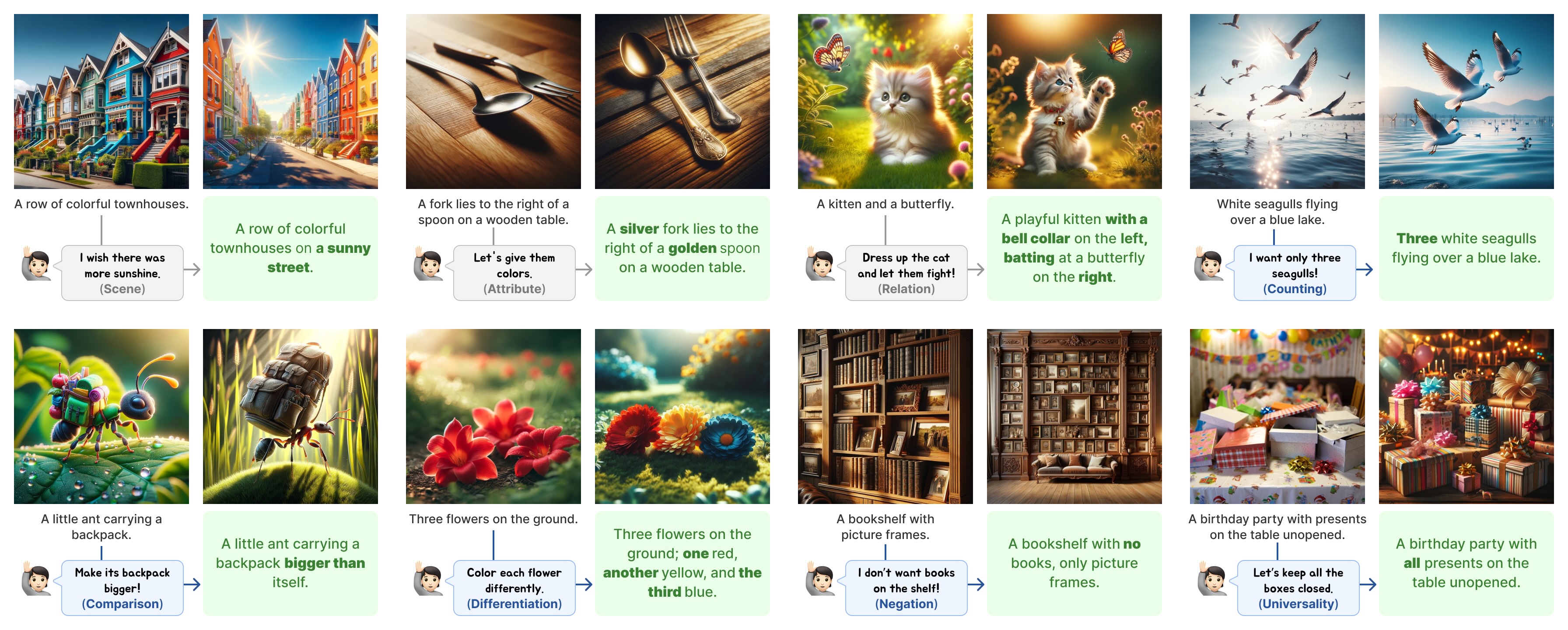

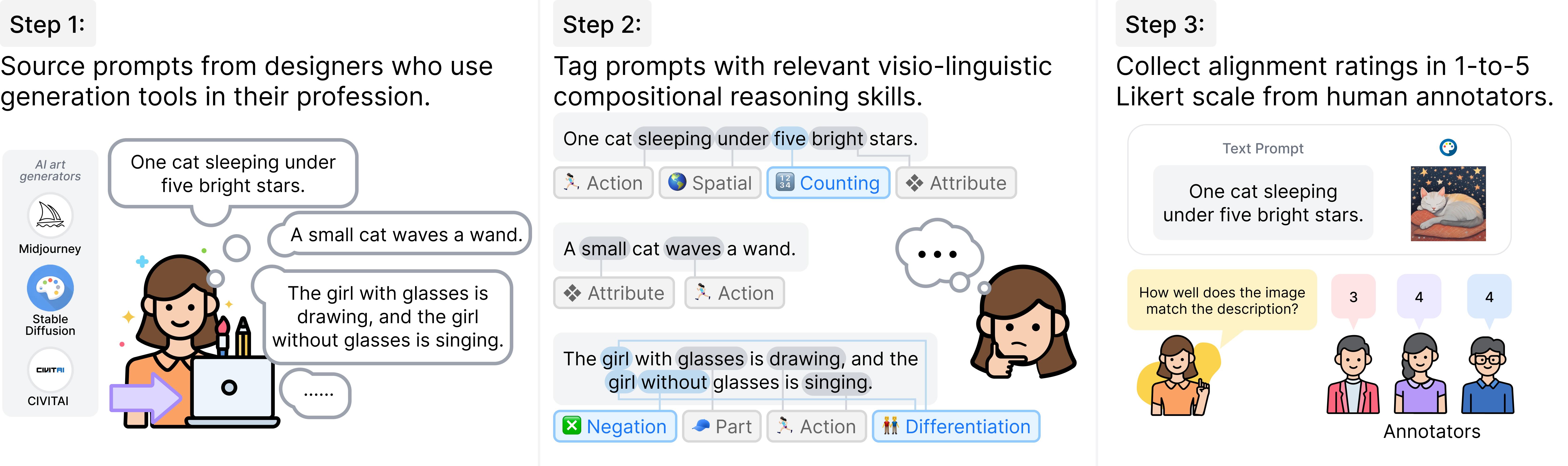

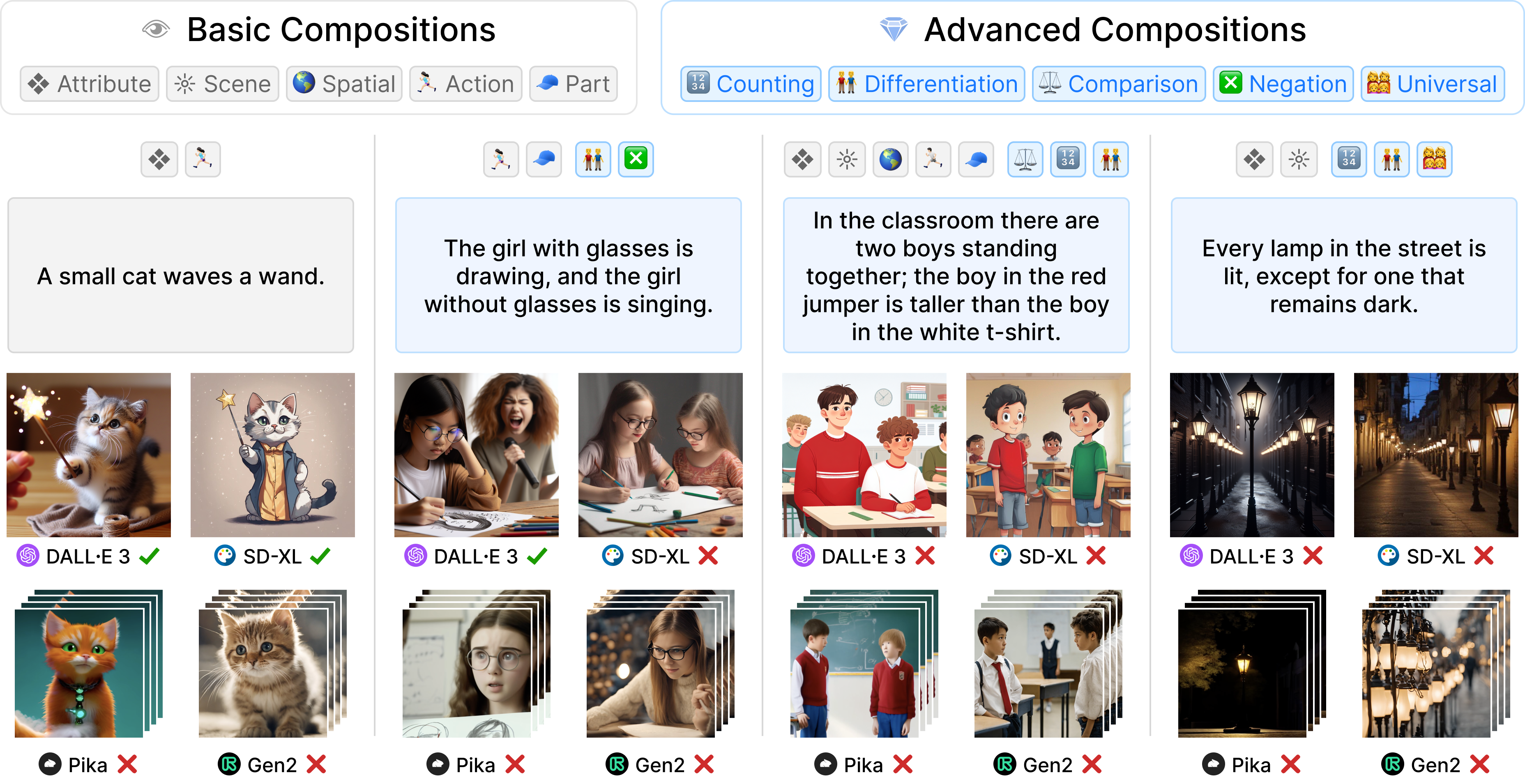

During our studies, we found that previous text-to-visual benchmarks like COCO and PartiPrompt lacked sufficiently challenging prompts. To address this, we collected 1,600 real prompts from graphic designers using tools like Midjourney. This results in GenAI-Bench [Li et al., CVPR 2024], which covers a broader range of compositional reasoning and presents a tougher challenge to text-to-visual models.

GenAI-Bench [Li et al., CVPR 2024] reflects how users seek precise control in text-to-visual generation using compositional prompts. For example, users often add details by specifying compositions of objects, scenes, attributes, and relationships (spatial/action/part). Additionally, user prompts may involve higher-order reasoning, including counting, comparison, differentiation, and logic (negation/universality).

After gathering these diverse, real-world prompts, we collected 1-to-5 Likert-scale ratings on the generated images from state-of-the-art models like Midjourney and Stable Diffusion, with three annotators evaluating each image-text pair. We also discuss in the paper how these human ratings can be used to better evaluate future automated metrics.

We collect prompts from professional designers to ensure GenAI-Bench reflects real-world needs. Designers write prompts on general topics (e.g., food, animals, household objects) without copyrighted characters or celebrities. We carefully tag each prompt with its evaluated skills and hire human annotators to rate images and videos generated by state-of-the-art models.

Importantly, we found that most models still struggle with GenAI-Bench prompts, indicating significant room for improvement:

State-of-the-art models such as DALL-E 3, SD-XL, Pika, and Gen2 still fail to handle compositional prompts of GenAI-Bench!

Improving Text-to-Image Generation with VQAScore

Lastly, we demonstrate how VQAScore can improve text-to-image generation in a black-box manner [Liu et al., CVPR 2024] by selecting the highest-VQAScore images from as few as three generated candidates:

VQAScore can improve DALL-E 3 on challenging GenAI-Bench prompts using its black-box API to rank the three generated candidate images. We encourage readers to refer to our paper for the full experimental setup and human evaluation results!

Conclusion

Metrics and benchmarks play a crucial role in the evolution of science. We hope that VQAScore and GenAI-Bench provide new insights into the evaluation of text-to-visual models and offer a robust, reproducible alternative to costly human evaluations.

References:

Lin et al., Evaluating Text-to-Visual Generation with Image-to-Text Generation. ECCV 2024.

Li et al., GenAI-Bench: Evaluating and Improving Compositional Text-to-Visual Generation. CVPR SynData 2024 Workshop, Best Short Paper.

Lin et al., Revisiting the Role of Language Priors in Vision-Language Models. ICML 2024.

Liu et al., Language Models as Black-Box Optimizers for Vision-Language Models. CVPR 2024.

Parashar et al., The Neglected Tails in Vision-Language Models. CVPR 2024.

Hessel et al., A Reference-free Evaluation Metric for Image Captioning. EMNLP 2021.

Heusel et al., GANs Trained by a Two Time-Scale Update Rule Converge to a Local Nash Equilibrium. NeurIPS 2017.

Betker et al., Improving Image Generation with Better Captions (DALL-E 3). OpenAI 2023.

Esser et al., Scaling Rectified Flow Transformers for High-Resolution Image Synthesis. Stability AI 2024.

Zhang et al., The Unreasonable Effectiveness of Deep Features as a Perceptual Metric. CVPR 2018.

Thrush et al., Winoground: Probing Vision and Language Models for Visio-Linguistic Compositionality. CVPR 2022.

Yuksekgonul et al., When and why vision-language models behave like bags-of-words, and what to do about it? ICLR 2023.

Advances in generative models have made it possible for AI-generated text, code, and images to mirror human-generated content in many applications. Watermarking, a technique that embeds information in the output of a model to verify its source, aims to mitigate the misuse of such AI-generated content. Current state-of-the-art watermarking schemes embed watermarks by slightly perturbing probabilities of the LLM’s output tokens, which can be detected via statistical testing during verification.

Unfortunately, our work shows that common design choices in LLM watermarking schemes make the resulting systems surprisingly susceptible to watermark removal or spoofing attacks—leading to fundamental trade-offs in robustness, utility, and usability. To navigate these trade-offs, we rigorously study a set of simple yet effective attacks on common watermarking systems and propose guidelines and defenses for LLM watermarking in practice.

Prompt

Alan Turing was born in …

Unwatermarked Z-Score: 0.16 ↓ PPL: 3.19

Alan Turing was born in1912 and diedin1954.He was anEnglishmathematician,logician, cryptanalyst,and computerscientist. In1938,Turing joinedthe Government Code and Cypher School (GC&CS), where hecontributed to the design of the bombe,a machinethat was usedto decipher the Enigma-enciphered messages…

Watermarked Z-Score: 5.98 ↑ PPL: 4.46

Alan Turing was born in1912 anddiedin 1954, attheage of41. He was the brilliant British scientist andmathematician whois largely credited with beingthefatherofmodern computer science. He is known for his contributions to mathematicalbiologyand chemistry. He was also one ofthepioneers of computerscience…

Alan Turing was born in1950and died in 1994, at the age of 43. He was the brilliant American scientist and mathematician who is largely credited with being the father of modern computer science. He is known for his contributions to mathematical biology and musicology. He was also one of the pioneers of computer science…

Alan Turing was born in1912 and died in 1954. He was a mathematician, logician, cryptologist and theoretical computer scientist. He is famous for his work on code-breaking and artificial intelligence, and his contribution to the Allied victory in World War II. Turing was born in London. He showed an interest in mathematics…

(c) Watermark-removal attack Exploiting public detection API Z-Score: 1.47 ↓ PPL: 4.57

Alan Turing was born in1912 and died in 1954. He was an English mathematician, computer scientist, cryptanalystand philosopher. Turing was a leading mathematicianand cryptanalyst. He was one of the key players in cracking the German Enigma Code during World War II. He also came up with the Turing Machine…

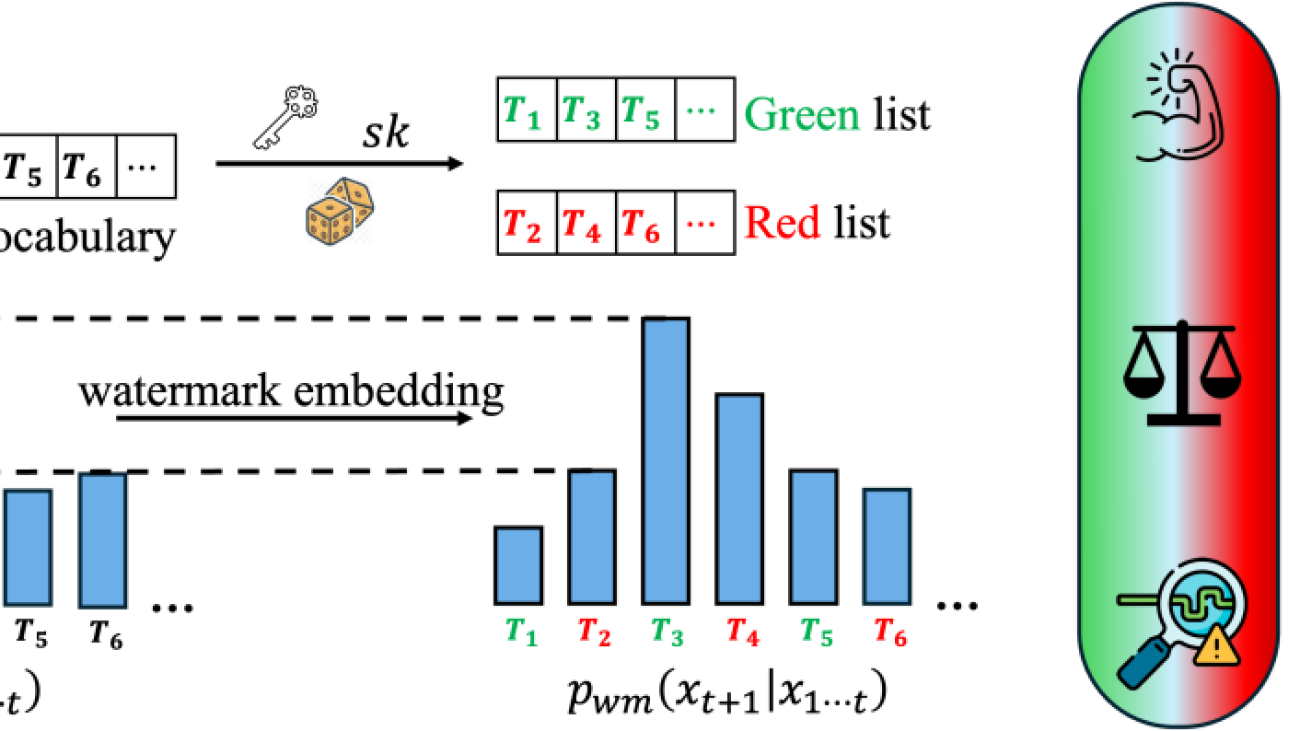

Table 1. Examples generated using LLAMA-2-7B with/without the KGW watermark under various attacks. The watermark will split the vocabulary into green and red lists and give preference for words in the green list. Z-score reflects the detection confidence of the watermark, and perplexity (PPL) measures text quality. (a) In the piggyback spoofing attack, we exploit watermark robustness by generating incorrect content that appears as watermarked (matching the z-score of the watermarked baseline), potentially damaging the reputation of the LLM. Incorrect tokens modified by the attacker are marked in orange and watermarked tokens in blue. (b-c) In watermark-removal attacks, attackers can effectively lower the z-score below the detection threshold while preserving a high sentence quality (low PPL) by exploiting either the (b) use of multiple keys or (c) publicly available watermark detection APIs.

What is LLM Watermarking?

Similar to image watermarks, LLM watermarking embeds invisible secret patterns into the text. Here, we briefly introduce LLMs and LLM watermarks. We use (x) to denote a sequence of tokens, (x_i in mathcal{V}) represents the (i)-th token in the sequence, and (mathcal{V}) is the vocabulary. (M_{text{orig}}) denotes the original model without a watermark, (M_{text{wm}}) is the watermarked model, and (sk in mathcal{S}) is the watermark secret key sampled from (mathcal{S}).

Language Model. State-of-the-art (SOTA) LLMs are auto-regressive models, which predict the next token based on the prior tokens. We define language models more formally below:

Definition 1 (Language Model). A language model (LM) without a watermark is a mapping: $$ M_{text{orig}}: mathcal{V}^* rightarrow mathcal{V}, $$ where the input is a sequence of length (t) tokens (x). (M_{text{orig}}(textbf{x})) first returns the probability distribution for the next token, then (x_{t+1}) is sampled from this distribution.

Figure 1. LLM predicts the next tokens auto-regressively.

Watermarks for LLMs. We focus on SOTA decoding-based robust watermarking schemes including KGW, Unigram, and Exp. In each of these methods, the watermarks are embedded by perturbing the output distribution of the original LLM. The perturbation is determined by secret watermark keys held by the LLM owner. Formally, we define the watermarking scheme:

Definition 2 (Watermarked LLMs). The watermarked LLM takes token sequence (x in mathcal{V}^* ) and secret key (sk in mathcal{S}) as input, and outputs a perturbed probability distribution for the next token. The perturbation is determined by (sk):

$$M_{text{wm}} : mathcal{V}^* times mathcal{S} rightarrow mathcal{V}$$

The watermark detection outputs the statistical testing score for the null hypothesis that the input token sequence is independent of the watermark secret key: $$f_{text{detection}} : mathcal{V}^* times mathcal{S} rightarrow mathbb{R}$$ The output score reflects the confidence of the watermark’s existence in the input.

Figure 2. Watermark is embedded by perturbing the probability distribution of the next token. The perturbation is determined by the secret key (sk).

Common Design Choices of LLM Watermarks

There are a number of common design choices in existing LLM watermarking schemes, including robustness, the use of multiple keys, and public detection APIs that have clear benefits to enhance watermark security and usability. We describe these key design choices briefly below, and then explain how an attacker can easily take advantage of these design choices to launch watermark removal or spoofing attacks.

Robustness. The goal of developing a watermark that is robust to output perturbations is to defend against watermark removal, which may be used to circumvent detection schemes for applications such as phishing or fake news generation. Robust watermark designs have been the topic of many recent works. A more robust watermark can better defend against watermark-removal attacks. However, our work shows that robustness can also enable piggyback spoofing attacks.

Multiple Keys. Many works have explored the possibility of launching watermark stealing attacks to infer the secret pattern of the watermark, which can then boost the performance of spoofing and removal attacks. A natural and effective defense against watermark stealing is using multiple watermark keys during embedding, which can improve the unbiasedness property of the watermark (it is called distortion-free in the Exp watermark). Rotating multiple secret keys is a common practice in cryptography and is also suggested by prior watermarks. More keys being used during embedding indicates better watermark unbiasedness and thus it becomes more difficult for attackers to infer the watermark pattern. However, we show that using multiple keys can also introduce new watermark-removal vulnerabilities.

Public Detection API. It is still an open question whether watermark detection APIs should be made publicly available to users. Although this makes it easier to detect watermarked text, it is commonly acknowledged that it will make the system vulnerable to attacks. We study this statement more precisely by examining the specific risk trade-offs that exist, as well as introducing a novel defense that may make the public detection API more feasible in practice.

Attacks, Defenses, and Guidelines

Although the above design choices are beneficial for enhancing the security and usability of watermarking systems, they also introduce new vulnerabilities. Our work studies a set of simple yet effective attacks on common watermarking systems and propose guidelines and defenses for LLM watermarking in practice.

In particular, we study two types of attacks—watermark-removal attacks and (piggyback or general) spoofing attacks. In the watermark-removal attack, the attacker aims to generate a high-quality response from the LLM without an embedded watermark. For the spoofing attacks, the goal is to generate a harmful or incorrect output that has the victim organization’s watermark embedded.

Piggyback Spoofing Attack Exploiting Robustness

More robust watermarks can better defend against editing attacks, but this seemingly desirable property can also be easily misused by malicious users to launch simple piggyback spoofing attacks. In piggyback spoofing attacks, a small portion of toxic or incorrect content is inserted into the watermarked material, making it seem like it was generated by a specific watermarked LLM. The toxic content will still be detected as watermarked, potentially damaging the reputation of the LLM service provider.

Attack Procedure. (i) The attacker queries the target watermarked LLM to receive a high-entropy watermarked sentence (x_{wm}), (ii) The attacker edits (x_{wm}) and forms a new piece of text (x’) and claims that (x’) is generated by the target LLM. The editing method can be defined by the attacker. Simple strategies could include inserting toxic tokens into the watermarked sentence (x_{wm}), or editing specific tokens to make the output inaccurate. As we show, editing can be done at scale by querying another LLM like GPT4 to generate fluent output.

Results. We show that piggyback spoofing can generate fluent, watermarked, but inaccurate results at scale. Specifically, we edit the watermarked sentence by querying GPT4 using the prompt "Modify less than 3 words in the following sentence and make it inaccurate or have opposite meanings."

Figure 3. Piggyback spoofing on KGW and LLAMA-2-7B. Lower perplexity (PPL) indicates higher sentence quality. Higher z-score reflects higher confidence in watermarking.

Figure 3 shows that we can successfully generate fluent results, with a slightly higher PPL. 94.17% of the piggyback results have a z-score higher than the detection threshold 4. We randomly sample 100 piggyback results and manually check that most of them (92%) are fluent and have inaccurate or opposite content from the original watermarked content. We present a spoofing sentence below. For more results, please check our manuscript.

Watermarked content, z-score: 4.93, PPL: 4.61 Earth has a history of 4.5 billion years and humans have been around for 200,000 years. Yet humans have been using computers for just over 70 years and even then the term was first used in 1945. In the age of technology, we are still just getting started. The first computer, ENIAC (Electronic Numerical Integrator And Calculator), was built at the University of Pennsylvania between 1943 and 1946. The ENIAC took up 1800 sq ft and had 18,000 vacuum tube and mechanical parts. The ENIAC was used for mathematical calculations, ballistics, and code breaking. The ENIAC was 1000 times faster than any other calculator of the time. The first computer to run a program was the Z3, built by Konrad Zuse at his house.

Piggyback attack, z-score: 4.36, PPL: 5.68 Earth has a history of 4.5 billion years and humans have been around for 200,000 years. Yet humans have been using computers for just over 700 years and even then the term was first used in 1445. In the age of technology, we are still just getting started. The first computer, ENIAC (Electronic Numerical Integrator And Calculator), was built at the University of Pennsylvania between 1943 and 1946. The ENIAC took up 1800 sq ft and had 18,000 vacuum tube and mechanical parts. The ENIAC was used for mathematical calculations, ballistics, and code breaking. The ENIAC was 1000 times slower than any other calculator of the time. The first computer to run a program was the Z3, built by Konrad Zuse at his house.

Discussion. Piggyback spoofing attacks are easy to execute in practice. Robust LLM watermarks typically do not consider such attacks during design and deployment, and existing robust watermarks are inherently vulnerable to such attacks. We consider this attack to be challenging to defend against, especially considering the examples presented above, where by only editing a single token, the entire content becomes incorrect. It is hard, if not impossible, to detect whether a particular token is from the attacker by using robust watermark detection algorithms. Recently, researchers proposed publicly detectable watermarks that plant a cryptographic signature into the generated sentence [Fairoze et al. 2024]. They mitigate such piggyback spoofing attacks at the cost of sacrificing robustness. Thus, practitioners should weigh the risks of removal vs. piggyback spoofing attacks for the model at hand.

Guideline #1. Robust watermarks are vulnerable to spoofing attacks and are not suitable as proof of content authenticity alone. To mitigate spoofing while preserving robustness, it may be necessary to combine additional measures such as signature-based fragile watermarks.

Watermark-Removal Attack Exploiting Multiple Keys

SOTA watermarking schemes aim to ensure the watermarked text retains its high quality and the private watermark patterns are not easily distinguished by maintaining an unbiasedness property: $$|mathbb{E}_{sk in mathcal{S}}[M_{text{wm}}(textbf{x}, sk)] – M_text{orig}(textbf{x})| = O(epsilon),$$ i.e., the expected distribution of watermarked output over the watermark key space (sk in S) is close to the output distribution without a watermark, differing by a distance of (epsilon). Exp is rigorously unbiased, and KGW and Unigram slightly shift the watermarked distributions.

We consider multiple keys to be used during watermark embedding to defend against watermark stealing attacks. The insight of our proposed watermark-removal attack is that, given the “unbiased” nature of watermarks, malicious users can estimate the output distribution without any watermark by repeatedly querying the watermarked LLM using the same prompt. As this attack estimates the original, unwatermarked distribution, the quality of the generated content is preserved.

Attack Procedure. (i) An attacker queries a watermarked model with an input (x) multiple times, observing (n) subsequent tokens (x_{t+1}). (ii) The attacker then creates a frequency histogram of these tokens and samples according to the frequency. This sampled token matches the result of sampling on an unwatermarked output distribution with a nontrivial probability. Consequently, the attacker can progressively eliminate watermarks while maintaining a high quality of the synthesized content.

Results. We study the trade-off between resistance against watermark stealing and watermark-removal attacks by evaluating a recent watermark stealing attack [Jovanović et al. 2024], where we query the watermarked LLM to obtain 2.2 million tokens to “steal” the watermark pattern and then launch spoofing attacks using the estimated watermark pattern. In our watermark removal attack, we consider that the attacker has observations with different keys.

Figure 4a. Z-Score and attack success rate (ASR) of watermark stealing on KGW watermark and LLAMA-2-7B model with different watermark keys (n).

Figure 4b. Z-Score and attack success rate (ASR) of watermark-removal on KGW watermark and LLAMA-2-7B model with different watermark keys (n).

Figure 4c. Perplexity (PPL) of watermark-removal on KGW watermark and LLAMA-2-7B model with different watermark keys (n).

As shown in Figure 4a, using multiple keys can effectively defend against watermark stealing attacks. With a single key, the ASR is 91%. We observe that using three keys can effectively reduce the ASR to 13%, and using more than 7 keys, the ASR of the watermark stealing is close to zero. However, using more keys also makes the system vulnerable to our watermark-removal attacks as shown in Figure 4b. When we use more than 7 keys, the detection scores of the content produced by our watermark removal attacks closely resemble those of unwatermarked content and are much lower than the detection thresholds, with ASRs higher than 97%. Figure 4c suggests that using more keys improves the quality of the output content. This is because, with a greater number of keys, there is a higher probability for an attacker to accurately estimate the unwatermarked distribution.

Discussion. Many prior works have suggested using multiple keys to defend against watermark stealing attacks. However, we reveal that a conflict exists between improving resistance to watermark stealing and the feasibility of removing watermarks. Our results show that finding a “sweet spot” in terms of the number of keys to use to mitigate both the watermark stealing and the watermark-removal attacks is not trivial. Given this tradeoff, we suggest that LLM service providers consider “defense-in-depth” techniques such as anomaly detection, query rate limiting, and user identification verification.

Guideline #2. Using a larger number of watermarking keys can defend against watermark stealing attacks, but increases vulnerability to watermark-removal attacks. Limiting users’ query rates can help to mitigate both attacks.

Attacks Exploiting Public Detection APIs

Fially, we show that publicly available detection APIs can enable both spoofing and removal attacks. The insight is that by querying the detection API, the attacker can gain knowledge about whether a specific token is carrying the watermark or not. Thus, the attacker can select the tokens based on the detection result to launch spoofing and removal attacks.

Attack Procedure. (i) An attacker feeds a prompt into the watermarked LLM (removal attack) or into a local LLM (spoofing attack), which generates the response in an auto-regressive manner. For the token (x_i) the attacker will generate a list of possible replacements for (x_i). (ii) The attacker will query the detection using these replacements and sample a token based on their probabilities and detection scores to remove or spoof the watermark while preserving a high output quality. This replacement list can be generated by querying the watermarked LLM, querying a local model, or simply returned by the watermarked LLM (e.g., enabled by OpenAI’s API top_logprobs=5).

Results. We evaluate the detection scores for both the watermark-removal and the spoofing attacks. Furthermore, for the watermark-removal attack, where the attackers care more about the output quality, we report the output PPL.

Figure 5a. Z-Score/P-Value of watermark removal using detection APIs on LLAMA-2-7B and different watermarks.

Figure 5b. The perplexity of watermark removal using detection APIs on LLAMA-2-7B and different watermarks.

Figure 5c. Z-Score/P-Value of watermark spoofing using detection APIs on LLAMA-2-7B and different watermarks.

As shown in Figure 5a and Figure 5b, watermark-removal attacks exploiting the detection API significantly reduce detection confidence while maintaining high output quality. For instance, for the KGW watermark on LLAMA-2-7B model, we achieve a median z-score of 1.43, which is much lower than the threshold 4. The PPL is also close to the watermarked outputs (6.17 vs. 6.28). We observe that the Exp watermark has higher PPL than the other two watermarks. A possible reason is that Exp watermark is deterministic, while other watermarks enable random sampling during inference. Our attack also employs sampling based on the token probabilities and detection scores, thus we can improve the output quality for the Exp watermark. The spoofing attacks also significantly boost the detection confidence even though the content is not from the watermarked LLM, as depicted in Figure 5c.

Defending Detection with Differential Privacy. In light of the issues above, we propose an effective defense using ideas from differential privacy (DP) to counteract the detection API based spoofing attacks. DP adds random noise to function results evaluated on private datasets such that the results from neighboring datasets are indistinguishable. Similarly, we consider adding Gaussian noise to the distance score in the watermark detection, making the detection ((epsilon, delta))-DP, and ensuring that attackers cannot tell the difference between two queries by replacing a single token in the content, thus increasing the hardness of launching the attacks.

Figure 6a. Spoofing attack success rate (ASR) and detection accuracy (ACC) without and with DP watermark detection under different noise parameters.

Figure 6b. Z-scores of original text without attack, spoofing attack without DP defense, and spoofing attacks with DP defense. We use the best (sigma=4) from Figure 6a.

As shown in Figure 6, with a noise scale of (sigma=4), the DP detection’s accuracy drops from the original 98.2% to 97.2% on KGW and LLAMA-2-7B, while the spoofing ASR becomes 0%. The results are consistent for other watermarks and models.

Discussion. The detection API, available to the public, aids users in differentiating between AI and human-created materials. However, it can be exploited by attackers to gradually remove watermarks or launch spoofing attacks. We propose a defense utilizing the ideas in differential privacy. Even though the attacker can still obtain useful information by increasing the detection sensitivity, our defense significantly increases the difficulty of spoofing attacks. However, this method is less effective against watermark-removal attacks that exploit the detection API because attackers’ actions will be close to random sampling, which, even though with lower success rates, remains an effective way of removing watermarks. Therefore, we leave developing a more powerful defense mechanism against watermark-removal attacks exploiting detection API as future work. We recommend companies providing detection services should detect and curb malicious behavior by limiting query rates from potential attackers, and also verify the identity of the users to protect against Sybil attacks.

Guideline #3. Public detection APIs can enable both spoofing and removal attacks. To defend against these attacks, we propose a DP-inspired defense, which combined with techniques such as anomaly detection, query rate limiting, and user identification verification can help to make public detection more feasible in practice.

Conclusion

Although LLM watermarking is a promising tool for auditing the usage of LLM-generated text, fundamental trade-offs exist in the robustness, usability, and utility of existing approaches. In particular, our work shows that it is easy to take advantage of common design choices in LLM watermarks to launch attacks that can easily remove the watermark or generate falsely watermarked text. Our study finds that these vulnerabilities are common to existing LLM watermarks and provides caution for the field in deploying current solutions in practice without carefully considering the impact and trade-offs of watermarking design choices. To establish more reliable future LLM watermarking systems, we also suggest guidelines for designing and deploying LLM watermarks along with possible defenses motivated by the theoretical and empirical analyses of our attacks. For more results and discussions, please see our manuscript.

A central question in the discussion of large language models (LLMs) concerns the extent to which they memorize their training data versus how they generalize to new tasks and settings. Most practitioners seem to (at least informally) believe that LLMs do some degree of both: they clearly memorize parts of the training data—for example, they are often able to reproduce large portions of training data verbatim [Carlini et al., 2023]—but they also seem to learn from this data, allowing them to generalize to new settings. The precise extent to which they do one or the other has massive implications for the practical and legal aspects of such models [Cooper et al., 2023]. Do LLMs truly produce new content, or do they only remix their training data? Should the act of training on copyrighted data be deemed an unfair use of data, or should fair use be judged by some notion of model memorization? When dealing with humans, we distinguish plagiarizing content from learning from it, but how should this extend to LLMs? The answer inherently relates to the definition of memorization for LLMs and the extent to which they memorize their training data.

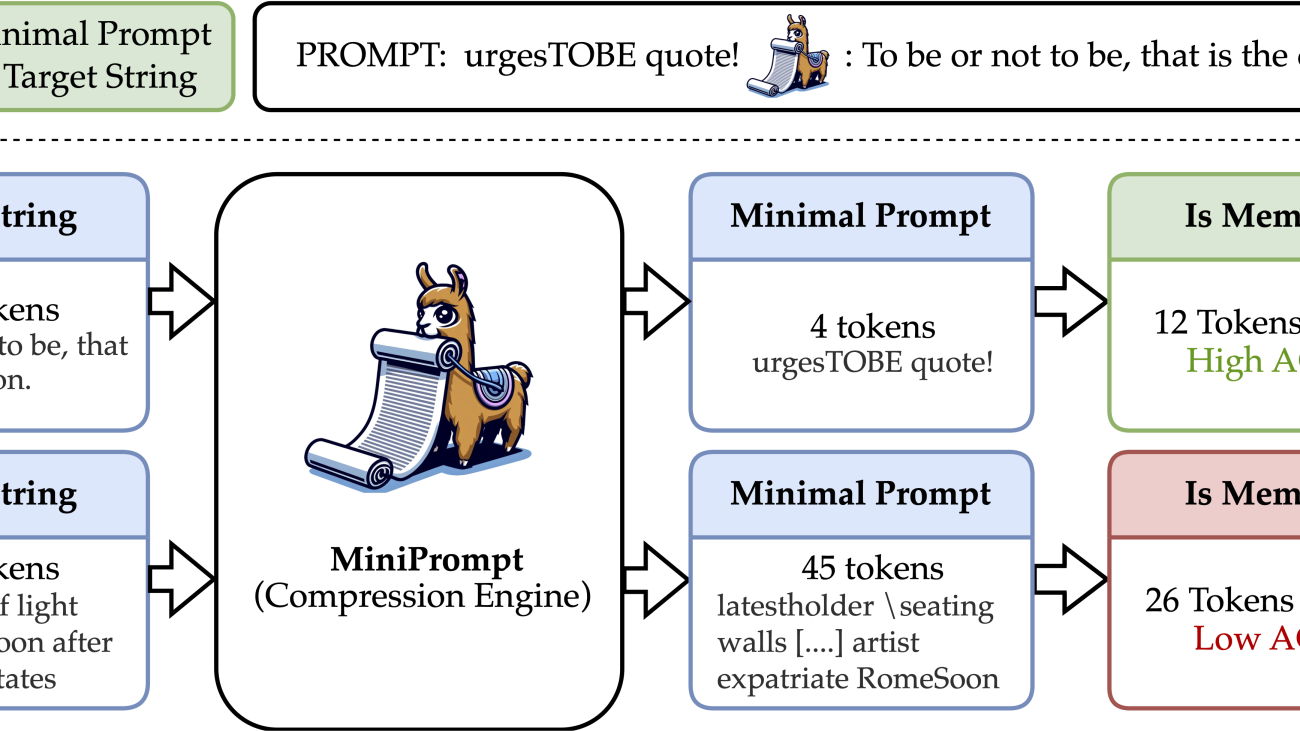

However, even defining memorization for LLMs is challenging, and many existing definitions leave much to be desired. In our recent paper (project page), we propose a new definition of memorization based on a compression argument. Our definition posits that

a phrase present in the training data is memorized if we can make the model reproduce the phrase using a prompt (much) shorter than the phrase itself.

Operationalizing this definition requires finding the shortest adversarial input prompt that is specifically optimized to produce a target output. We call this ratio of input-to-output tokens the Adversarial Compression Ratio (ACR). In other words, memorization is inherently tied to whether a certain output can be represented in a compressed form beyond what language models can do with typical text. We argue that such a definition provides an intuitive notion of memorization. If a certain phrase exists within the LLM training data (e.g., is not itself generated text) and it can be reproduced with fewer input tokens than output tokens, then the phrase must be stored somehow within the weights of the LLM. Although it may be more natural to consider compression in terms of the LLM-based notions of input/output perplexity, we argue that a simple compression ratio based on input/output token counts provides a more intuitive explanation to non-technical audiences and has the potential to serve as a legal basis for important questions about memorization and permissible data use. In addition to its intuitive nature, our definition has several other desirable qualities. We show that it appropriately ascribes many famous quotes as being memorized by existing LLMs (i.e., they have high ACR values). On the other hand, we find that text not in the training data of an LLM, such as samples posted on the internet after the training period, are not compressible, that is their ACR is low.

We examine several unlearning methods using ACR to show that they do not substantially affect the memorization of the model. That is, even after explicit finetuning, models asked to “forget” certain pieces of content are still able to reproduce them with a high ACR—in fact, not much smaller than with the original model. Our approach provides a simple and practical perspective on what memorization can mean, providing a useful tool for functional and legal analysis of LLMs.

Why We Need A New Definition

With LLMs ingesting more and more data, questions about their memorization are attracting attention [e.g., Carlini et al., 2019, 2023;Nasr et al., 2023;Zhang et al., 2023]. There remains a pressing need to accurately define memorization in a way that serves as a practical tool to ascertain the fair use of public data from a legal standpoint. To ground the problem, consider the court’s role in determining whether an LLM is breaching copyright. What constitutes a breach of copyright remains contentious, and prior work defines this on a spectrum from ‘training on a data point itself constitutes violation’ to ‘copyright violation only occurs if a model verbatim regurgitates training data.’ To formalize our argument for a new notion of memorization, we start with three definitions from prior work to highlight some of the gaps in the current thinking about memorization.

Discoverable memorization [Carlini et al., 2023], which says a string is memorized if the first few words elicit the rest of the quote exactly, has three particular problems. It is very permissive, easy to evade, and requires validation data to set parameters. Another notion is Extractable Memorization [Nasr et al., 2023], which says that if there exists a prompt that elicits the string in response. This falls too far on the other side of the issue by being very restrictive—what if the prompt includes the entire string in question, or worse, the instructions to repeat it? LLMs that are good at repeating will follow that instruction and output any string they are asked to. The risk is that it is possible to label any element of the training set as memorized, rendering this definition unfit in practice. Another definition is Counterfactual Memorization [Zhang et al., 2023], which aims to separate memorization from generalization and is tested through retraining many LLMs. Given the cost of training LLMs, such a definition is impractical for legal use.

In addition to these definitions from prior work on LLM memorization, several other seemingly viable approaches to memorization exist. Ultimately, we argue all of these frameworks—the definitions in existing work and the approaches described below—are each missing key elements of a good definition for assessing fair use of data.

Membership is not memorization. Perhaps if a copyrighted piece of data is in the training set at all, we might consider it a problem. However, there is a subtle but crucial difference between training set membership and memorization. In particular, the ongoing lawsuits in the field [e.g., as covered by Metz and Robertson, 2024] leave open the possibility that reproducing another’s creative work is problematic, but training on samples from that data may not be. This is common practice in the arts—consider that a copycat comedian telling someone else’s jokes is stealing, but an up-and-comer learning from tapes of the greats is doing nothing wrong. So while membership inference attacks (MIAs) [e.g. Shokri et al., 2017] may look like tests for memorization and they are even intimately related to auditing machine unlearning [Carlini et al., 2021, Pawelczyk et al., 2023, Choi et al., 2024], they have three issues as tests for memorization. Specifically, they are very restrictive, they are hard to arbitrate, and evaluation techniques are brittle.

Adversarial Compression Ratio

Our definition of memorization is based on answering the following question: Given a piece of text, how short is the minimal prompt that elicits that text exactly? In this section, we formally define and introduce our MiniPrompt algorithm that we use to answer our central question.

To begin, let a target natural text string (s) have a token sequence representation (xin mathcal V^*), which is a list of integer-valued indices that index a given vocabulary (mathcal V). We use (|cdot|) to count the length of a token sequence. A tokenizer (T:smapsto x) maps from strings to token sequences. Let (M) be an LLM that takes a list of tokens as input and outputs the next token probabilities. Consider that (M) can perform generation by repeatedly predicting the next token from all the previous tokens with the argmax of its output appended to the sequence at each step (this process is called greedy decoding). With a slight abuse of notation, we will also call the greedy decoding result the output of (M). Let (y) be the token sequence generated by (M), which we call a completion or response: (y = M(x)), which in natural language says that the model generates (y) when prompted with (x) or that (x) elicits (y) as a response from (M). So our compression ratio ACR is defined for a target sequence (y) as ACR((M, y) = frac{|y|}{|x^*|}), where (x^* = text{argmin}_{x} |x|) s.t. (M(x) = y).

Definition [(tau)-Compressible Memorization] Given a generative model (M), a sample (y) from the training data is (tau)-memorized if the ACR((M, y) > tau(y)).

The threshold (tau(y)) is a configurable parameter of this definition. We might choose to compare the ACR to the compression ratio of the text when run through a general-purpose compression program (explicitly assumed not to have memorized any such text) such as GZIP [Gailly and Adler, 1992] or SMAZ [Sanfilippo, 2006]. This amounts to setting (tau(y)) equal to the SMAZ compression ratio of (y), for example. Alternatively, one might even use the compression ratio of the arithmetic encoding under another LLM as a comparison point, for example, if it was known with certainty that the LLM was never trained on the target output and hence could not have memorized it [Delétang et al., 2023]. In reality, copyright attribution cases are always subjective, and the goal of this work is not to argue for the right threshold function but rather to advocate for the adversarial compression framework for arbitrating fair data use. Thus, we use (tau = 1), which we believe has substantial practical value. 1

Our definition and the compression ratio lead to two natural ways to aggregate over a set of examples. First, we can average the ratio over all samples/test strings and report the average compression ratio (this is (tau)-independent). Second, we can label samples with a ratio greater than one as memorized and discuss the portion memorized over some set of test cases (for our choice of (tau =1 )).

Empirical Findings

Model Size vs. Memorization: Since prior work has proposed alternative definitions of memorization that show that bigger models memorize more [Carlini et al., 2023], we ask whether our definition leads to the same finding. We find the same trends under our definition, meaning our view of memorization is consistent with existing scientific findings.

Unlearning for Privacy: We further experiment with models finetuned on synthetic data, which show that completion-based tests (i.e., the model’s ability to generate a specific output) often fail to fully reflect the model’s memorization. However, the ACR captures the persistence of memorization even after moderate attempts at unlearning.

Four Categorties of Data for Validation: We also validate the ACR as a metric using four different types of data: random sequences, famous quotes, Wikipedia sentences, and recent Associated Press (AP) articles. The goal is to ensure that the ACR aligns with intuitive expectations of memorization. Our results show that random sequences and recent AP articles, which the models were not trained on, are not compressible (i.e., not memorized). Famous quotes, which are repeated in the training data, show high compression ratios, indicating memorization. Wikipedia sentences fall between the two extremes, as some of them are memorized. These results validate that ACR meaningfully identifies memorization in data that is more common or repeated in the training set, while appropriately labelling unseen data as not-memorized.

When proposing new definitions, we are tasked with justifying why a new one is needed as well as showing its ability to capture a phenomenon of interest. This stands in contrast to developing detection/classification tools whose accuracy can easily be measured using labeled data. It is difficult by nature to define memorization as there is no set of ground truth labels that indicate which samples are memorized. Consequently, the criteria for a memorization definition should rely on how useful it is. Our definition is a promising direction for future regulation on LLM fair use of data as well as helping model owners confidently release models trained on sensitive data without releasing that data. Deploying our framework in practice may require careful thought about how to set the compression threshold but as it relates to the legal setting this is not a limitation as law suits always have some subjectivity [Downing, 2024]. Furthermore, as evidence in a court, this metric would not provide a binary test on which a suit could be decided, rather it would be a piece of a batch of evidence, in which some is more probative than others. Our hope is to provide regulators, model owners, and the courts a mechanism to measure the extent to which a model contains a particular string within its weights and make discussion about data usage more grounded and quantitative.

References

Nicholas Carlini, Chang Liu, Úlfar Erlingsson, Jernej Kos, and Dawn Song. The secret sharer: Evaluating and testing unintended memorization in neural networks. In 28thUSENIX security symposium (USENIX security 19), pages 267–284, 2019.

Nicholas Carlini, Steve Chien, Milad Nasr, Shuang Song, Andreas Terzis, and Florian Tramer. Membership inference attacks from first principles. arXiv preprint arXiv:2112.03570, 2021.

Nicholas Carlini, Daphne Ippolito, Matthew Jagielski, Katherine Lee, Florian Tramer, and Chiyuan Zhang. Quantifying memorization across neural language models, 2023.

Dami Choi, Yonadav Shavit, and David K Duvenaud. Tools for verifying neural models’ training data. Advances in Neural Information Processing Systems, 36, 2024.

A Feder Cooper, Katherine Lee, James Grimmelmann, Daphne Ippolito, Christo- pher Callison-Burch, Christopher A Choquette-Choo, Niloofar Mireshghallah, Miles Brundage, David Mimno, Madiha Zahrah Choksi, et al. Report of the 1st workshop on generative ai and law. arXiv preprint arXiv:2311.06477, 2023.

Grégoire Delétang, Anian Ruoss, Paul-Ambroise Duquenne, Elliot Catt, Tim Genewein, Christopher Mattern, Jordi Grau-Moya, Li Kevin Wenliang, Matthew Aitchison, Laurent Orseau, et al. Language modeling is compression. arXiv preprint arXiv:2309.10668, 2023.

Kate Downing. Copyright fundamentals for AI researchers. In Proceedings of the Twelfth International Conference on Learning Representations (ICLR), 2024. URL https://iclr.cc/media/iclr-2024/Slides/21804.pdf.

Jean-Loup Gailly and Mark Adler. gzip. https://www.gnu.org/software/gzip/, 1992. Accessed: 2024-05-21.

Cade Metz and Katie Robertson. Openai seeks to dismiss parts of the new york times’s lawsuit. The New York Times, 2024. URL https://www.nytimes.com/2024/02/27/ technology/openai-new-york-times-lawsuit.html#: ̃:text=In%20its%20suit% 2C%20The%20Times,someone%20to%20hack%20their%20chatbot.

Milad Nasr, Nicholas Carlini, Jonathan Hayase, Matthew Jagielski, A Feder Cooper, Daphne Ippolito, Christopher A Choquette-Choo, Eric Wallace, Florian Tram`er, and Katherine Lee. Scalable extraction of training data from (production) language models. arXiv preprint arXiv:2311.17035, 2023.

Martin Pawelczyk, Seth Neel, and Himabindu Lakkaraju. In-context unlearning: Language models as few shot unlearners. arXiv preprint arXiv:2310.07579, 2023.

Reza Shokri, Marco Stronati, Congzheng Song, and Vitaly Shmatikov. Membership inference attacks against machine learning models. In 2017 IEEE symposium on security and privacy (SP), pages 3–18. IEEE, 2017.

Chiyuan Zhang, Daphne Ippolito, Katherine Lee, Matthew Jagielski, Florian Tramèr, and Nicholas Carlini. Counterfactual memorization in neural language models. Advances in Neural Information Processing Systems, 36:39321–39362, 2023.

Footnotes

1 There exist prompts like “count from (1) to (1000),” for which a chat model (M) is able to generate (1, 2, ldots, 1000),” which results in a very high ACR. However, for copyright purposes, we argue that this category of algorithmic prompts is in the gray area where determining memorization is difficult and beyond the scope of this paper, given our primary application to creative works.

Causal inference is the process of determining whether and how a cause leads to an effect, typically using statistical methods to distinguish correlation from causation. Learning causal relationships from data is an important task across a wide variety of domains ranging from healthcare and drug development, to online advertising and e-commerce. As a result, there has been much work in the literature on economics, statistics, computer science, and public policy on designing algorithms and methodologies for causal inference.

While most of the focus has been on questions which are statistical in nature, one must also take game-theoretic incentives into consideration when doing causal inference about strategic individuals who have a preference over the treatment they receive. For example, it may be hard to infer causal relationships in randomized control trials when there is non-compliance by participants in the study (i.e. when participants do not adhere to the treatment they are assigned). More generally, causal learning may be difficult whenever individuals are free to self-select their own treatments and there is sufficient heterogeneity between individuals with different preferences. Even when compliance can be enforced, individuals may strategize by modifying the attributes they present to the causal inference process in order to be assigned a more desirable treatment.

This annotated reading list is intended to serve as a brief summary of work on causal inference in the presence of strategic agents. While this list is not comprehensive, we hope that it will be a useful starting point for members of the machine learning community to learn more about this exciting research area at the intersection of causal inference and game theory.

The reading list is organized as follows: (1, 3) study non-compliance in randomized trials, (2-4) focus on instrumental variable methods, (4-6) consider incentive misalignment between the individual running the causal inference procedure and the subjects of the procedure, (7,8) study cross-unit interference, and (9,10) are about synthetic control methods.

[Robins 1998]: This paper provides an overview of methods to correct for non-compliance in randomized trials (i.e., non-adherence by trial participants to the treatment assignment protocol).

[Angrist et al. 1996]: This seminal paper outlines the concept of instrumental variables (IVs) and describes how they can be used to estimate causal effects. An IV is a variable that affects the treatment variable but is unrelated to the outcome variable except through its effect on the treatment. IV methods leverage the fact that variation in IVs is independent of any confounding in order to estimate the causal effect of the treatment.

[Ngo et al. 2021]: Unlike prior work on non-compliance in clinical trials, this work leverages tools from information design to reveal information about the effectiveness of the treatments in such a way that participants become incentivized to comply with the treatment recommendations over time.

[Harris et al. 2022]: This paper studies the problem of making decisions about a population of strategic agents. The authors make the novel observation that the assessment rule deployed by the principal is a valid instrument, which allows them to apply standard methods for instrumental variable regression to learn causal relationships in the presence of strategic behavior.

[Miller et al. 2020]: This paper considers the problem of strategic classification, where a principal (i.e. decision maker) makes decisions about a population of strategic agents. Given knowledge of the principal’s deployed assessment rule, the agents may strategically modify their observable features in order to receive a more desirable assessment (e.g., a better interest rate on a loan). The authors are the first to show that designing good incentives for agent improvement (i.e. encouraging strategizing in a way which actually benefits the agent) is at least as hard as orienting edges in the corresponding causal graph.

[Wang et al. 2023]: Incentive misalignment between patients and providers may occur when average treated outcomes are used as quality metrics. Such misalignment is generally undesirable in healthcare domains, as it may lead to decreased patient welfare. To mitigate this issue, this work proposes an alternative quality metric, the total treatment effect, which accounts for counterfactual untreated outcomes. The authors show that rewarding the total treatment effect maximizes total patient welfare.

[Wager and Xu 2021]: Motivated by applications such as ride-sharing and tuition subsidies, this work studies settings in which interventions on one unit (e.g. a person or product) may have effects on others (i.e., cross-unit interference). The authors focus on the problem of setting supply-side payments in a centralized marketplace. They use a mean-field modeling-based approach to model the cross-unit interference, and design a class of experimentation schemes which allow them to optimize payments without disturbing the market equilibrium.

[Li et al. 2023]: Like [Wager and Xu 2021], this paper studies the effects of cross-unit interference, although the interference considered here comes from congestion in a service system. As a result, the interference considered here is dynamic, in contrast to the static interference considered in the previous entry.

[Abadie and Gardeazabal 2003]: This is the first paper on synthetic control methods (SCMs), a popular technique for estimating counterfactuals from longitudinal data. In the SCM setup, there is a pre-intervention time period during which all units are under control, followed by a post-intervention time period when all units undergo exactly one intervention (either the treatment or control). Given a test unit (who was given the treatment) and a set of donor units (who remained under control), SCMs use the pre-treatment data to learn a relationship (usually linear or convex) between the test and donor units. This relationship is then extrapolated to the post-intervention time period in order to estimate the counterfactual trajectory for the test unit under control.

[Ngo et al. 2023]: A common assumption in the literature on SCMs is that of “overlap”: the outcomes for the test unit can be written as a combination (e.g., linear or convex) of the donor units. This work sheds light on this often overlooked assumption and shows that (i) when units select their own treatments and (ii) there is sufficient heterogeneity between units who prefer different treatments, then overlap does not hold. Like [Ngo et al. 2021], the authors use tools from information design and multi-armed bandits to incentivize units to explore different treatments in a way which ensures that the overlap condition will gradually become satisfied over time.

Recently, our CMU-MATH team proudly clinched 2nd place in the Artificial Intelligence Mathematical Olympiad (AIMO) out of 1,161 participating teams, earning a prize of $65,536! This prestigious competition aims to revolutionize AI in mathematical problem-solving, with the ultimate goal of building a publicly-shared AI model capable of winning a gold medal in the International Mathematical Olympiad (IMO). Dive into our blog to discover the winning formula that set us apart in this significant contest.

Background: The AIMO competition

The Artificial Intelligence Mathematical Olympiad (AIMO) Prize, initiated by XTX Markets, is a pioneering competition designed to revolutionize AI’s role in mathematical problem-solving. It pushes the boundaries of AI by solving complex mathematical problems akin to those in the International Mathematical Olympiad (IMO). The advisory committee of AIMO includes Timothy Gowers and Terence Tao, both winners of the Fields Medal. Attracting attention from world-class mathematicians as well as machine learning researchers, the AIMO sets a new benchmark for excellence in the field.

AIMO has introduced a series of progress prizes. The first of these was a Kaggle competition, with the 50 test problems hidden from competitors. The problems are comparable in difficulty to the AMC12 and AIME exams for the USA IMO team pre-selection. The private leaderboard determined the final rankings, which then determined the distribution of $253,952 in the one-million dollar prize pool among the top five teams. Each submitted solution was allocated either a P100 GPU or 2xT4 GPUs, with up to 9 hours to solve the 50 problems.

Just to give an idea about how the problems look like, AIMO provided a 10-problem training set open to the public. Here are two example problems in the set:

Let (k, l > 0) be parameters. The parabola (y = kx^2 – 2kx + l) intersects the line (y = 4) at two points (A) and (B). These points are distance 6 apart. What is the sum of the squares of the distances from (A) and (B) to the origin?

Each of the three-digits numbers (111) to (999) is coloured blue or yellow in such a way that the sum of any two (not necessarily different) yellow numbers is equal to a blue number. What is the maximum possible number of yellow numbers there can be?

The first problem is about analytic geometry. It requires the model to understand geometric objects based on textual descriptions and perform symbolic computations using the distance formula and Vieta’s formulas. The second problem falls under extremal combinatorics, a topic beyond the scope of high school math. It’s notoriously challenging because there’s no general formula to apply; solving it requires creative thinking to exploit the problem’s structure. It’s non-trivial to master all these required capabilities even for humans, let alone language models.

In general, the problems in AIMO were significantly more challenging than those in GSM8K, a standard mathematical reasoning benchmark for LLMs, and about as difficult as the hardest problems in the challenging MATH dataset. The limited computational resources—P100 and T4 GPUs, both over five years old and much slower than more advanced hardware—posed an additional challenge. Thus, it was crucial to employ appropriate models and inference strategies to maximize accuracy within the constraints of limited memory and FLOPs.

Our winning formula

Unlike most teams that relied on a single model for the competition, we utilized a dual-model approach. Our final solutions were derived through a weighted majority voting system, which consists of generating multiple solutions with a policy model, assigning a weight to each solution using a reward model, and then choosing the answer with the highest total weight. Specifically, we paired a policy model—designed to generate problem solutions in the form of computer code—with a reward model—which scored the outputs of the policy model. Our final solutions were derived through a weighted majority voting system, where the answers were generated by the policy model and the weights were determined by the scores from the reward model. This strategy stemmed from our study on compute-optimal inference, demonstrating that weighted majority voting with a reward model consistently outperforms naive majority voting given the same inference budget.

Both models in our submission were fine-tuned from the DeepSeek-Math-7B-RL checkpoint. Below, we detail the fine-tuning process and inference strategies for each model.

Policy model: Program-aided problem solver based on self-refinement

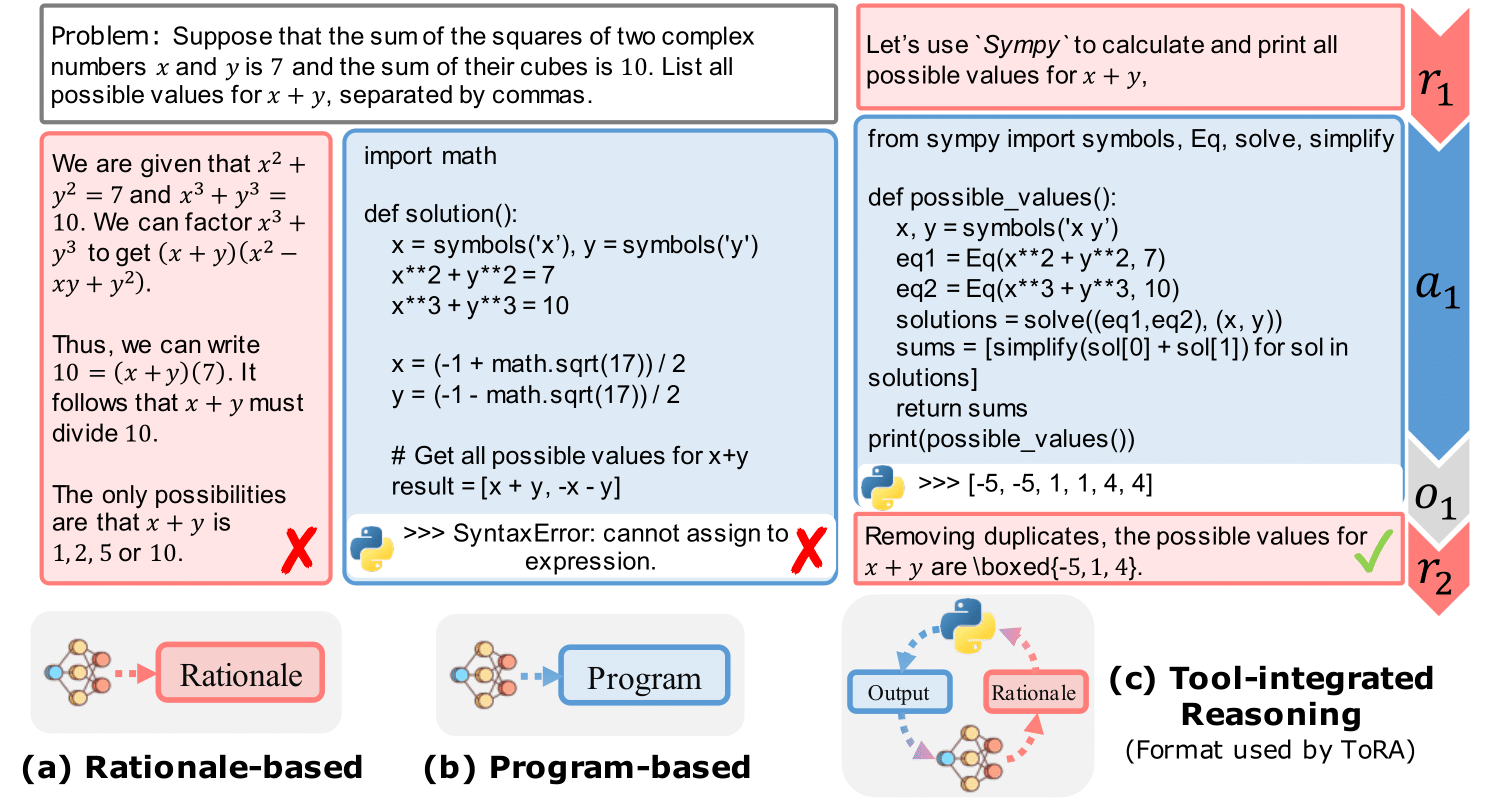

The policy model served as the primary problem solver in our approach. We noted that LLMs can perform mathematical reasoning using both text and programs. Natural language excels in abstract reasoning but falls short in precise computation, symbolic manipulation, and algorithmic processing. Programs, on the other hand, are adept at rigorous operations and can leverage specialized tools like equation solvers for complex calculations. To harness the benefits of both methods, we implemented the Program-Aided Language Models (PAL) or more precisely Tool-Augmented Reasoning (ToRA) approach, originally proposed by CMU & Microsoft. This approach combines natural language reasoning with program-based problem-solving. The model first generates rationales in text form, followed by a computer program which executes to derive a numerical answer

Figure 1: The tool-integrated reasoning format (from ToRA paper)

To train the model, we needed a suitable problem set (the given “training set” of this competition is too small for fine-tuning) with “ground truth” solutions in ToRA format for supervised fine-tuning. Given the problem difficulty (comparable to AMC12 and AIME exams) and the special format (integer answers only), we used a combination of AMC, AIME, and Odyssey-Math as our problem set, removing multiple-choice options and filtering out problems with non-integer answers. This resulted in a dataset of 2,600 problems. We prompted GPT-4o (and DeepSeek-Coder-V2) with few-shot examples to generate 64 solutions for each problem, retaining those that led to correct answers. Our final dataset contained 41,160 problem-solution pairs. We performed supervised fine-tuning on the open-sourced DeepSeek-Math-7B-RL model for 3 epochs with a learning rate of 2e-5.

During inference, we employed the self-refinement technique (which is another widely adopted technique proposed by CMU!), providing feedback to the policy model on the execution results of the generated program (e.g., invalid output, execution failure) and allowing the model to refine the solution accordingly.

Below we present our ablation study on the techniques we employed for the policy model. We used the accuracy on a selected subset of the MATH test set as the evaluation metric. It’s easy to see the combination of techniques that lead to large performance gains compared with naive baselines.

Model

Output format

Inference strategy

Accuracy

DeepSeek RL 7b

Text-only

Greedy decoding

54.02%

DeepSeek RL 7b

ToRA

Greedy decoding

58.05%

DeepSeek RL 7b

ToRA

Greedy + Self-refine

60.73%

DeepSeek RL 7b

ToRA

Maj@16 + Self-refine

70.46%

DeepSeek RL 7b

ToRA

Maj@64 + Self-refine

72.48%

Our finetuned model

ToRA

Maj@16 + Self-refine

74.50%

Our finetuned model

ToRA

Maj@64 + Self-refine

76.51%

Table: Ablation study of our techniques on a selected MATH subset (in which the problems are similar to AIMO problems). Maj@(n) denotes majority voting over (n) sampled solutions.

Notably, the first-place team also used ToRA with self-refinement. However, they curated a much larger problem set of 60,000 problems and used GPT-4 to generate solutions in the ToRA format. Their dataset was more than 20x larger than ours. The cost to generate solutions was far beyond our budget as an academic team (over $100,000 based on our estimation). Our problem set was based purely on publicly available data, and we spent only ~$1,000 for solution generation.

Reward model: Solution scorer using label-balance training

While the policy model was a creative problem solver, it could sometimes hallucinate and produce incorrect solutions. On the publicly available 10-problem training set, our policy model only correctly solved two problems using standard majority voting with 32 sampled solutions. Interestingly, for another 2 problems, the model generated correct solutions that failed to be selected due to wrong answers dominating in majority voting.

This observation highlighted the potential of the reward model. The reward model was a solution scorer that took the policy model’s output and generated a score between 0 and 1. Ideally, it assigned high scores to correct solutions and low scores to incorrect ones, aiding in the selection of correct answers during weighted majority voting.

The reward model was fine-tuned from a DeepSeek-Math-7B-RL model on a labeled dataset containing both correct and incorrect problem-solution pairs. We utilized the same problem set as for the policy model training and expanded it by incorporating problems from the MATH dataset with integer answers. Simple as it may sound, generating high-quality data and training a strong reward model was non-trivial. We considered the following two essential factors for the reward model training set:

Label balance: The dataset should contain both correct (positive examples) and incorrect solutions (negative examples) for each problem, with a balanced number of correct and incorrect solutions.

Diversity: The dataset should include diverse solutions for each problem, encompassing different correct approaches and various failure modes.

Sampling solutions from a single model cannot meet those factors. For example, while our fine-tuned policy model achieved very high accuracy on the problem set, it was unable to generate any incorrect solutions and lacked diversity amongst correct solutions. Conversely, sampling from a weaker model, such as DeepSeek-Math-7B-Base, rarely yielded correct solutions. To create a diverse set of models with varying capabilities, we employed two novel strategies:

Interpolate between strong and weak models. For MATH problems, we interpolated the model parameters of a strong model (DeepSeek-Math-7B-RL) and a weak model (DeepSeek-Math-7B-Base) to get models with different level of capabilities. Denote by (mathbf{theta}_{mathrm{strong}}) and (mathbf{theta}_{mathrm{weak}}) the model parameters of the strong and weak model. We considered interpolated models with parameters (mathbf{theta}_{alpha}=alphamathbf{theta}_{mathrm{strong}}+(1-alpha)mathbf{theta}_{mathrm{weak}}) and set (alphain{0.3, 0.4, cdots, 1.0}), obtaining 8 models. Those models exhibited different problem solving accuracies on MATH. We sampled two solutions from each model for each problem, yielding diverse outputs with balanced correct and incorrect solutions. This technique was motivated by the research on model parameter merging (e.g., model soups) and represented an interesting application of this idea, i.e., generating models with different levels of capabilities.

Leverage intermediate checkpoints. For the AMC, AIME, and Odyssey, recall that our policy model had been fine-tuned on those problems for 3 epochs. The final model and its intermediate checkpoints naturally provided us with multiple models exhibiting different levels of accuracy on these problems. We leveraged these intermediate checkpoints, sampling 12 solutions from each model trained for 0, 1, 2, and 3 epochs.

These strategies allowed us to obtain a diverse set of models almost for free, sampling varied correct and incorrect solutions. We further filtered the generated data by removing wrong solutions with non-integer answers since it was trivial to determine that those answers are incorrect during inference. In addition, for each problem, we maintained equal numbers of correct and incorrect solutions to ensure label balance and avoid a biased reward model. The final dataset contains 7000 unique problems and 37880 labeled problem-solution pairs. We finetuned DeepSeek-Math-7B-RL model for 2 epochs with learning rate 2e-5 on the curated dataset.

Figure 2: Weighted majority voting system based on the policy and reward models.

We validated the effectiveness of our reward model on the public training set. Notably, by pairing the policy model with the reward model and applying weighted majority voting, our method correctly solved 4 out of the 10 problems – while a single policy model could only solve 2 using standard majority voting.

Concluding remarks: Towards machine-based mathematical reasoning

With the models and techniques described above, our CMU-MATH team solved 22 out of 50 problems in the private test set, snagging the second place and establishing the best performance of an academic team. This outcome marks a significant step towards the goal of machine-based mathematical reasoning.

However, we also note that the accuracy achieved by our models still trails behind that of proficient human competitors who can easily solve over 95% of AIMO problems, indicating substantial room for improvement. There are a wide range of directions to be explored:

Advanced inference-time algorithms for mathematical reasoning. Our dual-model approach is a robust technique to enhance model reasoning at inference time. Recent research from our team suggests that more advanced inference-time algorithms, e.g., tree search methods, could even surpass weighted majority voting. Although computational constraints limited our ability to deploy this technique in the AIMO competition, future explorations on optimizing these inference-time algorithms can potentially lead to better mathematical reasoning approaches.

Integration of Automated Theorem Proving. Integrating automated theorem proving (ATP) tools, such as Lean, represents another promising frontier. ATP tools can provide rigorous logical frameworks and support for deeper mathematical analyses, potentially elevating the precision and reliability of problem-solving strategies employed by LLMs. The synergy between LLMs and ATP could lead to breakthroughs in complex problem-solving scenarios, where deep logical reasoning is essential.

Leveraging Larger, More Diverse Datasets. The competition reinforced a crucial lesson about the pivotal role of data in machine learning. Rich, diverse datasets, especially those comprising challenging mathematical problems, are vital for training more capable models. We advocate for the creation and release of larger datasets focused on mathematical reasoning, which would not only benefit our research but also the broader AI and mathematics communities.

Finally, we would like to thank Kaggle and XTX Markets for organizing this wonderful competition. We have open-sourced our code and datasets used in our solution to ensure reproducibility and facilitate future research. We invite the community to explore, utilize, and build upon our work, which is available in our GitHub repository. For further details about our results, please feel free to reach out to us!

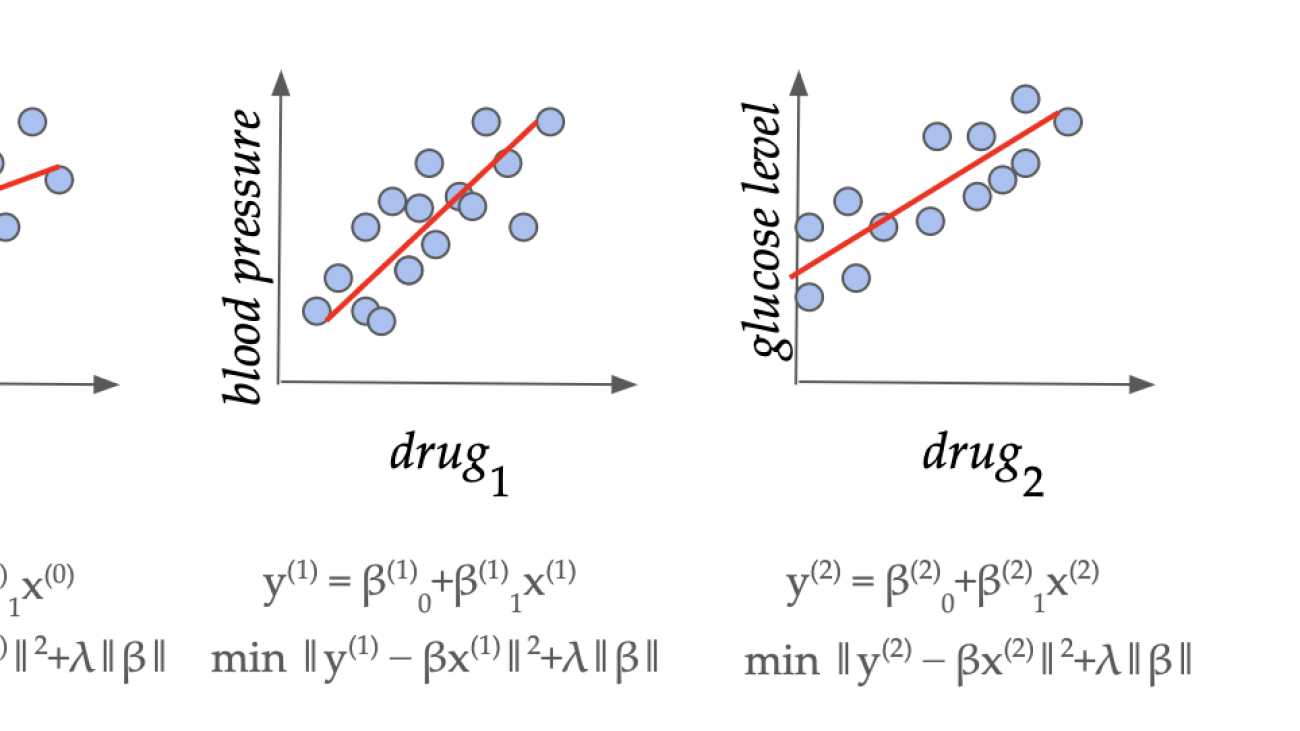

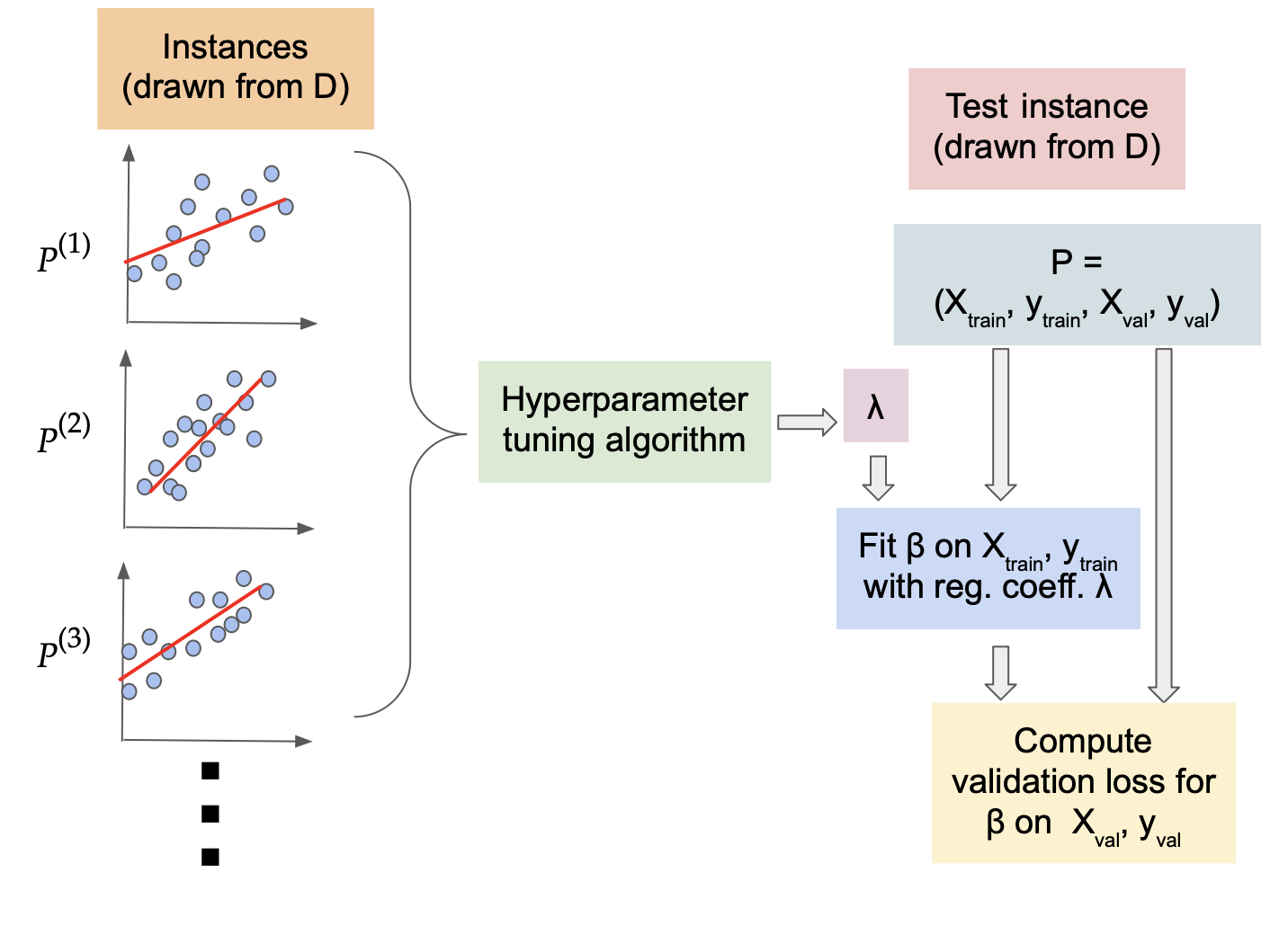

A series of regression instances in a pharmaceutical application. Can we learn how to set the regularization parameter (lambda) from similar domain-specific data?

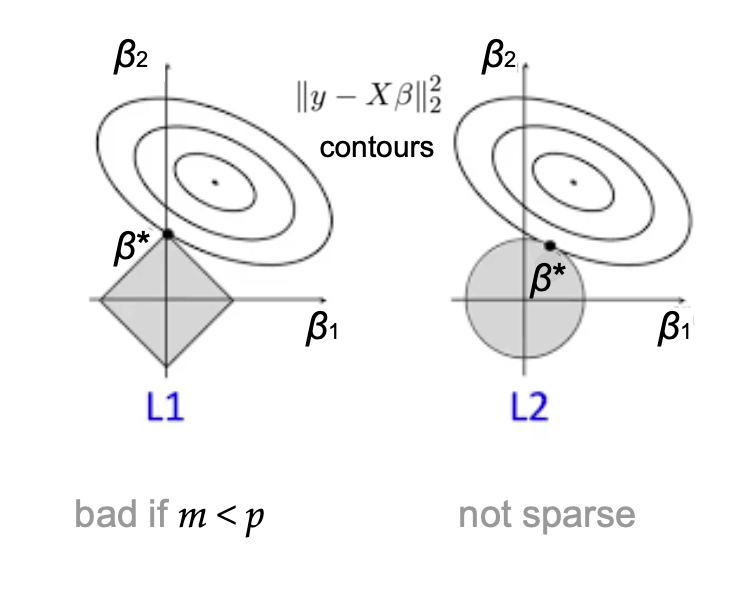

Overview. Perhaps the simplest relation between a real dependent variable (y) and a vector of features (X) is a linear model (y = beta X). Given some training examples or datapoints consisting of pairs of features and dependent variables ((X_1, y_1),(X_2, y_2),dots,(X_m,y_m)), we would like to learn (beta) which would give the best prediction (y’) given features (X’) of an unseen example. This process of fitting a linear model (beta) to the datapoints is called linear regression. This simple yet effective model finds ubiquitous applications, ranging from biological, behavioral, and social sciences to environmental studies and financial forecasting, to make reliable predictions on future data. In ML terminology, linear regression is a supervised learning algorithm with low variance and good generalization properties. It is much less data-hungry than typical deep learning models, and performs well even with small amounts of training data. Further, to avoid overfitting the model to the training data, which reduces the prediction performance on unseen data, one typically uses regularization, which modifies the objective function of the linear model to reduce impact of outliers and irrelevant features (read on for details).

The most common method for linear regression is “regularized least squares”, where one finds the (beta) which minimizes

$$||y – beta X||_2^2 + lambda ||beta||.$$

Here the first term captures the error of (beta) on the training set, and the second term is a norm-based penalty to avoid overfitting (e.g. reducing impact of outliers in data). How to set (lambda) appropriately in this fundamental method depends on the data domain and is a longstanding open question. In typical modern applications, we have access to several similar datasets (X^{(0)},y^{(0)}, X^{(1)},y^{(1)}, dots) from the same application domain. For example, there are often multiple drug trial studies in a pharmaceutical company for studying the different effects of similar drugs. In this work, we show that we can indeed learn a good domain-specific value of (lambda) with strong theoretical guarantees of accuracy on unseen datasets from the same domain, and give bounds on how much data is needed to achieve this.

As our main result, we show that if the data has (p) features (i.e., the dimension of feature vector (X_i) is (p), then after seeing (O(p/epsilon^2)) datasets, we can learn a value of (lambda) which has error (averaged over the domain) within (epsilon) of the best possible value of (lambda) for the domain. We also extend our results to sequential data, binary classification (i.e. (y) is binary valued) and non-linear regression.

Problem Setup. Linear regression with norm-based regularization penalty is one of the most popular techniques that one encounters in introductory courses to statistics or machine learning. It is widely used for data analysis and feature selection, with numerous applications including medicine, quantitative finance (the linear factor model), climate science, and so on. The regularization penalty is typically a weighted additive term (or terms) of the norms of the learned linear model (beta), where the weight is carefully selected by a domain expert. Mathematically, a dataset has dependent variable (y) consisting of (m) examples, and predictor variables (X) with (p) features for each of the (m) datapoints. The linear regression approach (with squared loss) consists of solving a minimization problem

where the highlighted term is the regularization penalty. Here (lambda_1, lambda_2ge 0) are the regularization coefficients constraining the L1 and L2 norms, respectively, of the learned linear model (beta). For general (lambda_1) and (lambda_2) the above algorithm is popularly known as the Elastic Net, while setting (lambda_1 = 0) recovers Ridge regression and setting (lambda_2 = 0) corresponds to LASSO. Ridge and LASSO regression are both individually popular methods in practice, and the Elastic Net incorporates the advantages of both.

Despite the central role these coefficients play in linear regression, the problem of setting them in a principled way has been a challenging open problem for several decades. In practice, one typically uses “grid search” cross-validation, which involves (1) splitting the dataset into several subsets consisting of training and validation sets, (2) training several models (corresponding to different values of regularization coefficients) on each training set, and (3) comparing the performance of the models on the corresponding validation sets. This approach has several limitations.

First, this is very computationally intensive, especially with the large datasets that typical modern applications involve, as one needs to train and evaluate the model for a large number of hyperparameter values and training-validation splits. We would like to avoid repeating this cumbersome process for similar applications.